General Liability Insurance is a type of business insurance that provides coverage for a variety of common risks and liabilities faced by businesses in the United States. It is designed to protect businesses from financial losses arising from claims related to bodily injury, property damage, personal injury, and advertising injury.

Here are some key points about General Liability Insurance:

Coverage: General Liability Insurance typically covers the costs associated with third-party claims or lawsuits alleging bodily injury or property damage caused by the business operations, products, or services. It can also cover claims related to personal injury, such as libel, slander, or copyright infringement. The policy may include coverage for legal defense costs, settlements, and judgments.

Types of Claims Covered: General Liability Insurance can cover a wide range of claims, including slip-and-fall accidents, property damage caused by the business or its employees, advertising-related claims, product liability claims, and certain types of professional errors or negligence.

Policy Limits: General Liability Insurance policies have coverage limits, which specify the maximum amount the insurer will pay for a covered claim. The policyholder is typically responsible for any costs exceeding those limits.

General liability insurance (GLI) can help cover claims that your business caused bodily injury or property damage. This coverage is also known as commercial general liability insurance (CGL). You can get GLI as a standalone policy or bundle it with other key coverages through a Business Owner’s Policy (BOP).

We’re here to help you understand what business liability insurance coverages your company may need. Whether it’s learning what general liability insurance covers or getting a general liability insurance quote, we’re here to help.

What Does General Liability Insurance Cover?

General liability insurance helps cover costly claims that can come up during normal business operations. If you don’t have coverage, you’d have to pay for these general liability insurance costs out of pocket.

In addition to GLI, there are other types of liability insurance that most insurance companies recommend:

1. Commercial umbrella insurance provides additional limits on top of some of your existing liability policies to help pay for expensive claims.

2. Employment practices liability insurance can help cover your legal defense costs and settlements or judgments if a current or former employee sues you for employment-related harassment, discrimination or wrongful termination.

3. Management liability insurance helps protect your business’ directors and officers from costly claims.

Commercial auto insurance helps protect you and your employees on the road if you’re driving a car for business.

Liability claims aren’t uncommon and can get expensive. In fact, 4 out of 10 small businesses will likely experience a liability claim in the next 10 years.** Slips and falls are the leading cause of emergency room visits.1 The average cost of this kind of claim is $35,000. If a claim leads to a lawsuit, it can increase its average cost to more than $75,000 to defend and settle.** Without general liability insurance, your business would have to pay for these costs out of pocket and it can put you out of business.

You may also need general liability insurance before you can work with other businesses. Some companies may ask you to provide proof of insurance, also known as a certificate of insurance.

Even though every business is unique, each one can benefit from having general liability coverage. We can work with you to customize your policy so you get the coverage amounts that are right for your business.

We’re backed by more than 200 years of experience and have helped over 1 million small business owners. We’re here to do the same for yours. We can help answer the question of “what is general liability coverage?” If you’re looking for a quote, trying to find out what your business’ general liability class code is or need help going through the claims process, our specialists are here for you. Our team consistently receives top scores for customer satisfaction in general liability insurance reviews, so you can have peace of mind knowing we’ve got your back.

General liability insurance is a type of liability insurance coverage that helps protect your business from claims that it caused bodily injuries or property damage to others. Without general liability coverage, you’d have to pay for these claims out of pocket. General liability insurance (GLI) is sometimes called business liability insurance or commercial general liability insurance or comprehensive general liability (CGL).

1. Health Insurance: Comprehensive health insurance coverage that includes medical, dental, and vision care can help employees access necessary healthcare services and reduce their out-of-pocket expenses.

2. Retirement Plans: Offering retirement plans, such as a 401(k) or pension plan, can help employees save for their future and provide them with a sense of financial security.

3. Life Insurance: Life insurance coverage provides financial protection to employees' beneficiaries in the event of their death. It can help ease the financial burden on loved ones and provide peace of mind.

4. Disability Insurance: Disability insurance provides income replacement if an employee becomes disabled and is unable to work. It helps protect employees' financial well-being during periods of disability.

5. Paid Time Off (PTO): Providing a generous PTO policy allows employees to take time off for vacations, personal reasons, or illness without experiencing a loss of income.

6. Flexible Work Arrangements: Offering flexible work arrangements, such as remote work options or flexible hours, can enhance work-life balance and improve employee morale.

7. Employee Assistance Programs (EAP): EAPs provide confidential counseling and support services to employees and their families to address personal or work-related issues, including mental health concerns.

8. Wellness Programs: Wellness programs promote employees' physical and mental well-being through initiatives like fitness memberships, health screenings, stress management programs, and educational resources.

9. Tuition Assistance: Providing tuition assistance or reimbursement programs can support employees' professional growth and development by helping them pursue further education or training.

10 Employee Discounts: Offering discounts on company products or services, as well as partnerships with local businesses, can enhance employee satisfaction and foster a sense of loyalty.

A customer enters a place of business where the floors have recently been cleaned and polished, and as a result, are very slippery. The customer slips on the floor and breaks a leg.

One of the employees of an electrical company visits a home for an electrical wiring job and accidentally causes a fire in the customer's home.

An advertisement placed by the business results in an individual claiming libel or slander.

Commercial general liability insurance covers injuries to a person or property damage that occurs on the premises of a business. This type of policy can also protect a business from claims of slander, libel, or advertising injury.

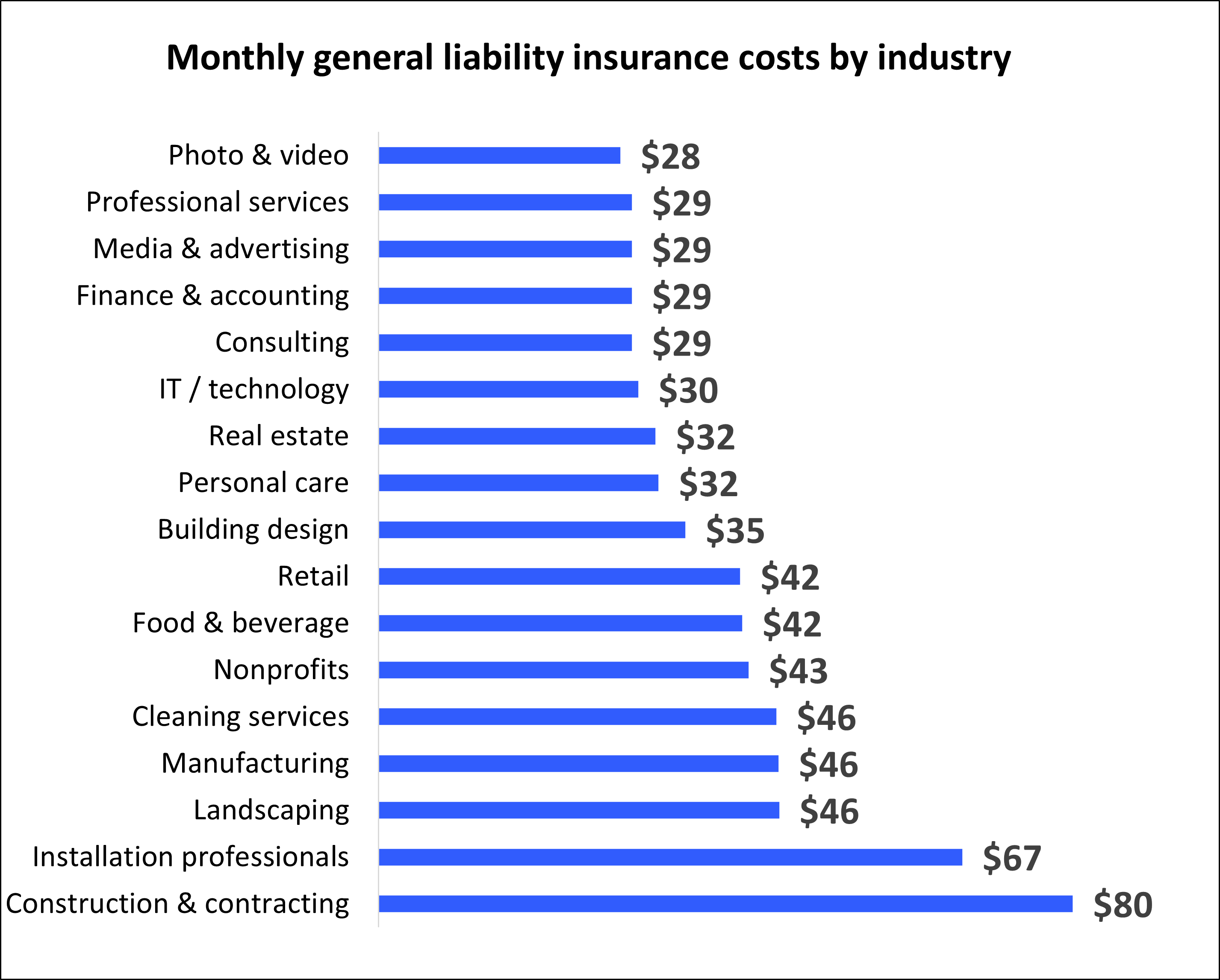

Naturally, the cost of commercial general liability Insurance will depend on the size of the business being insured, the riskiness of its business operations, and the amount of coverage needed. Some insurers say that their clients pay between $300 and $600 for a million dollars of insurance coverage. Others say their clients may pay as much as $1,000.

Most CGL policies do not cover intentional or expected damage by the insured. They also do not cover damages due to intoxication (in alcohol-related businesses), pollution, automobiles or other vehicles, damage to a business' work, or additional liabilities that the insured might take on. A business that is involved in these types of risks should purchase additional insurance in order to be fully covered.

Q: What are the coverages under general liability insurance?

A general liability insurance policy offers compensation for claims arising due to bodily injuries, and property damages or for which your business is accountable. This coverage is provided to the Owners of a company, or managing directors, operations heads, etc. who are involved in the business operations.

Q: What is the purpose of CGL?

Commercial general liability (CGL) is a type of insurance policy that provides coverage to a business for bodily injury, personal injury, and property damage caused by the business's operations, products, or injuries that occur on the business's premises.

Q: What line of business is general liability?

Commercial General Liability (CGL) policy covers third party liabilities arising from various business operations, be it premises, products and completed operations and/or advertising and personal injury.

Q: Is general liability insurance mandatory in India?

CGL insurance is not mandatory in India, but it is highly recommended for businesses to safeguard themselves against potential legal liability that may arise from their operations. The policy is suitable for businesses of all sizes and types, including small businesses, startups, and large corporations.

Q: What is a CGL policy?

Commercial General Liability (CGL) insurance protects business owners against claims of liability for bodily injury, property damage, and personal and advertising injury (slander and false advertising).

Q: What is double insurance?

Double insurance. Previous Next. (1) Where two or more policies are effected by or on behalf of the assured on the same adventure and interest or any part thereof, and the sums insured exceed the indemnity allowed by this Act, the assured is said to be over-insured by double insurance.

Q: What is CGL and E&O policy?

The CGL insurance covers bodily injury and physical property damage suffered by a third party, and E&O insurance covers financial loss suffered as a result of mistakes and poor professional advice.

Q: What is D&O and E&O policy?

D&O is there to protect high-level decision makers when someone asserts they were negligent in their duties as an officer or board member. E&O, on the other hand, covers acts, errors, and omissions committed by employees of the company.

Q: Can we take two insurance?

Having two insurance policies for your four-wheeler is not illegal in India. However, it is also not advisable to buy car insurance from two different companies. A single insurance company does not offer two different policies for the same car.

Q: What are the 2 types of insurance?

General Insurance. Following are the various types of general insurance in India: Health Insurance. Motor Insurance. Home Insurance.

Life Insurance. Following are several types of life insurance available in India: Term insurance. Term insurance with return of premium.

Q: Can a person have 2 types of insurance?

Having dual coverage is perfectly legal—you just need to coordinate your two benefits correctly to ensure your medical expenses are covered compliantly. If you're new to dual insurance, you've come to the right place!

Q: What is general liability insurance?

A: General liability insurance is a type of insurance coverage that provides protection to businesses and individuals against claims for bodily injury, property damage, personal injury, and advertising injury. It helps cover the costs associated with legal defense, settlements, and judgments in case someone sues you or your business for alleged negligence or harm caused by your products, services, or operations.

Q: Who needs general liability insurance?

A: General liability insurance is essential for businesses of all sizes and across various industries. It is particularly important for businesses that interact with clients, customers, or the public, as it helps protect against potential liability claims. Contractors, retailers, restaurants, professional service providers, and manufacturers are just a few examples of businesses that can benefit from having general liability insurance.

Q: What does general liability insurance typically cover?

A: General liability insurance typically covers the following:

Bodily injury: If someone is injured on your premises or due to your business operations, general liability insurance can cover medical expenses, legal fees, and potential settlements or judgments resulting from the injury.

Property damage: If you or your business causes damage to someone else's property, general liability insurance can help cover the repair or replacement costs.

Personal and advertising injury: General liability insurance can provide coverage for claims related to defamation, libel, slander, copyright infringement, false advertising, or other similar offenses.

Legal defense costs: General liability insurance can help cover the costs of hiring a lawyer, investigation expenses, court fees, and other legal expenses if you are sued. It's important to note that the coverage limits and specific terms of a general liability insurance policy can vary, so it's crucial to review the policy details and consult with an insurance professional to ensure you have the appropriate coverage for your specific needs.

Q: Is general liability insurance mandatory?

A: General liability insurance is not typically required by law. However, certain industry regulations, contracts, or lease agreements may mandate businesses to carry general liability insurance. Additionally, many businesses choose to obtain general liability insurance to protect their assets, reputation, and financial well-being in case of unforeseen accidents or lawsuits.

Q: How much does general liability insurance cost?

A: The cost of general liability insurance varies depending on factors such as the size and type of business, industry risks, coverage limits, location, and claims history. Premiums can range from a few hundred dollars to several thousand dollars per year. It's recommended to obtain multiple quotes from different insurance providers and work with an insurance professional to determine the appropriate coverage and obtain accurate cost estimates.

Q: Can general liability insurance cover professional errors or negligence?

A: No, general liability insurance typically does not cover errors, omissions, or negligence in professional services. For that type of coverage, professionals such as doctors, lawyers, architects, and consultants may need to consider professional liability insurance (also known as errors and omissions insurance), which is specifically designed to protect against professional mistakes or negligence claims.

Q: What is general insurance liability?

A: General liability insurance policies typically cover you and your company for claims involving bodily injuries and property damage resulting from your products, services or operations. It may also cover you if you are held liable for damages to your landlord's property.

Q: Who is an insured in CGL policy?

A limited liability company, you are an insured. Your members are also insureds, but only with respect to the conduct of your business. Your man- agers are insureds, but only with respect to their duties as your managers.

Q: How many limits are found in a CGL policy?

The CGL policy lists on the declarations six different limits. While the limits are separately listed, it is important to recognize that the limits are all interrelated. That is, payment of damages on one limit will also affect another limit

Q: What is the purpose of CGL?

Commercial general liability (CGL) is a type of insurance policy that provides coverage to a business for bodily injury, personal injury, and property damage caused by the business's operations, products, or injuries that occur on the business's premises.

Q: What is the GL limit?

The general aggregate limit applies to the total amount insurance companies will pay for covered losses during the policy period. If you reach the limit before the end of your policy period and there's another claim, you'll have to cover the costs out of pocket.

Q: What is GL in billing?

A general ledger, or GL, is a means for keeping record of a company's total financial accounts. Accounts typically recorded in a GL include: assets, liabilities, equity, expenses, and income or revenue.

Q: What is GL payroll?

The General Ledger provides an accounting summary to aid you or your bookkeeper with inputting a journal entry into your accounting software. The GL report we provide initially shows the credits/debits with default expense account names.

Copyright © FOLKSINFO.com.2023 All Rights Reserved

Powerd By ![]()